Blended family estate planning is a beautiful milestone, but it also creates a complex web of financial and legal obligations that standard estate planning simply wasn’t built to handle. If you rely on a generic “I love you will” – a plan where you leave everything to your new spouse, assuming they will eventually pass it on to your children – you may be putting your family’s future at risk.

Without a customized strategy, the consequences can be significant. You risk unintentionally disinheriting your own children, leaving your current spouse financially vulnerable, or accidentally enriching an ex-spouse due to outdated paperwork. Furthermore, ambiguity can spark legal disputes that disrupt your newly blended family the moment you are gone.

Protecting everyone you love doesn’t happen by accident; it requires deliberate, proactive legal planning. Navigating these overlapping obligations means moving beyond default state laws to create a well-structured strategy. Let’s explore the unique challenges blended families face and the essential legal tools available to protect your legacy and secure your family’s peace of mind.

What Is a Blended Family – and Why Does It Complicate Pennsylvania Estate Planning?

In the context of estate planning, a blended family generally refers to a household where at least one spouse has children from a previous relationship.

The primary complication arises from competing financial interests. You naturally want to ensure your current spouse is comfortable and financially secure after you pass away. Simultaneously, you want to help guarantee that the assets you have built over your lifetime are eventually passed down to your own children. Relying on default legal frameworks or generic planning tools often forces these two goals to clash.

Here is a quick look at why standard estate planning often falls short for blended families:

| Feature | Traditional Family Estate Planning | Blended Family Estate Planning |

| Primary Goal | Pass assets to the surviving spouse, then equally to shared children. | Balance the financial needs of a current spouse with the inheritance rights of children from a prior relationship. |

| Asset Ownership | Joint tenancy is standard and usually safe. | Joint tenancy can be risky in certain blended family situations, as it often bypasses children from a previous relationship entirely. |

| Trust Utilization | Simple wills may be sufficient in straightforward cases. | Specialized trusts are frequently required to control the timing and destination of assets. |

| Ex-Spouse Risk | Generally non-existent. | High risk if beneficiary designations or divorce decrees are not carefully reviewed and updated. |

The Biggest Risks Blended Families Face Without a Proper Estate Plan

When estate planning is neglected or handled with generic online forms, the outcomes for blended families can be highly problematic. Here are the most significant risks you face without specialized legal guidance.

Your Spouse Could Unintentionally Disinherit Your Children

If you leave your entire estate to your new spouse outright, those assets become their sole property. Even if your spouse promises to leave a portion of their estate to your children, circumstances can change. Your children could be completely disinherited if your surviving spouse:

- Remarries and decides to leave the assets to their new partner.

- Faces severe creditor issues or medical bankruptcies.

- Simply changes their will later in life, excluding your children.

Your Ex-Spouse Could End Up With Your Assets

Many people inadvertently forget to update their beneficiary designations after a divorce. While Pennsylvania law in many cases revokes beneficiary designations to an ex-spouse upon divorce, risks may still exist depending on circumstances, federal exceptions (like certain ERISA retirement plans), or outdated documents. If you fail to update your paperwork, your assets may pass directly to your ex–spouse, depending on the asset type and governing law, regardless of what your will says. Common assets at high risk include:

- Life insurance policies

- 401(k)s, pensions, and other retirement accounts

- Individual Retirement Accounts (IRAs)

Family Conflict and Legal Disputes After You Are Gone

Ambiguity is often a leading cause of estate litigation. If your wishes are not explicitly detailed in legally binding documents, your spouse and your children may find themselves in conflict over the interpretation of your intentions. This often leads to fractured family relationships and expensive probate disputes that reduce the estate’s overall value.

How Pennsylvania Law Treats Blended Families by Default

If you pass away without a will in Pennsylvania, you die “intestate,” and state law dictates how your assets are distributed. The default rules for blended families rarely align with a person’s actual wishes.

Under Pennsylvania intestacy laws, your surviving spouse does not automatically inherit your entire estate. Instead, the exact distribution depends on your family structure. The law typically triggers the following division:

- Your spouse generally receives an initial statutory amount (which is currently $30,000 under Pennsylvania law, but may change over time) plus one-half of the remaining intestate estate.

- Your children from a previous relationship generally divide the other half of the remaining estate.

While this may sound fair in theory, it often creates practical challenges, such as:

- Co-ownership conflicts: Your spouse and children may suddenly co-own the family home, potentially forcing a sale that leaves your surviving spouse looking for a new place to live.

- The “Elective Share”: Even if you write a will leaving everything to your children, Pennsylvania law grants a surviving spouse the right to claim an “elective share” of one-third of certain qualifying assets, as defined under Pennsylvania’s elective share rules, subject to specific calculation rules and estate composition, which may supersede your written wishes.

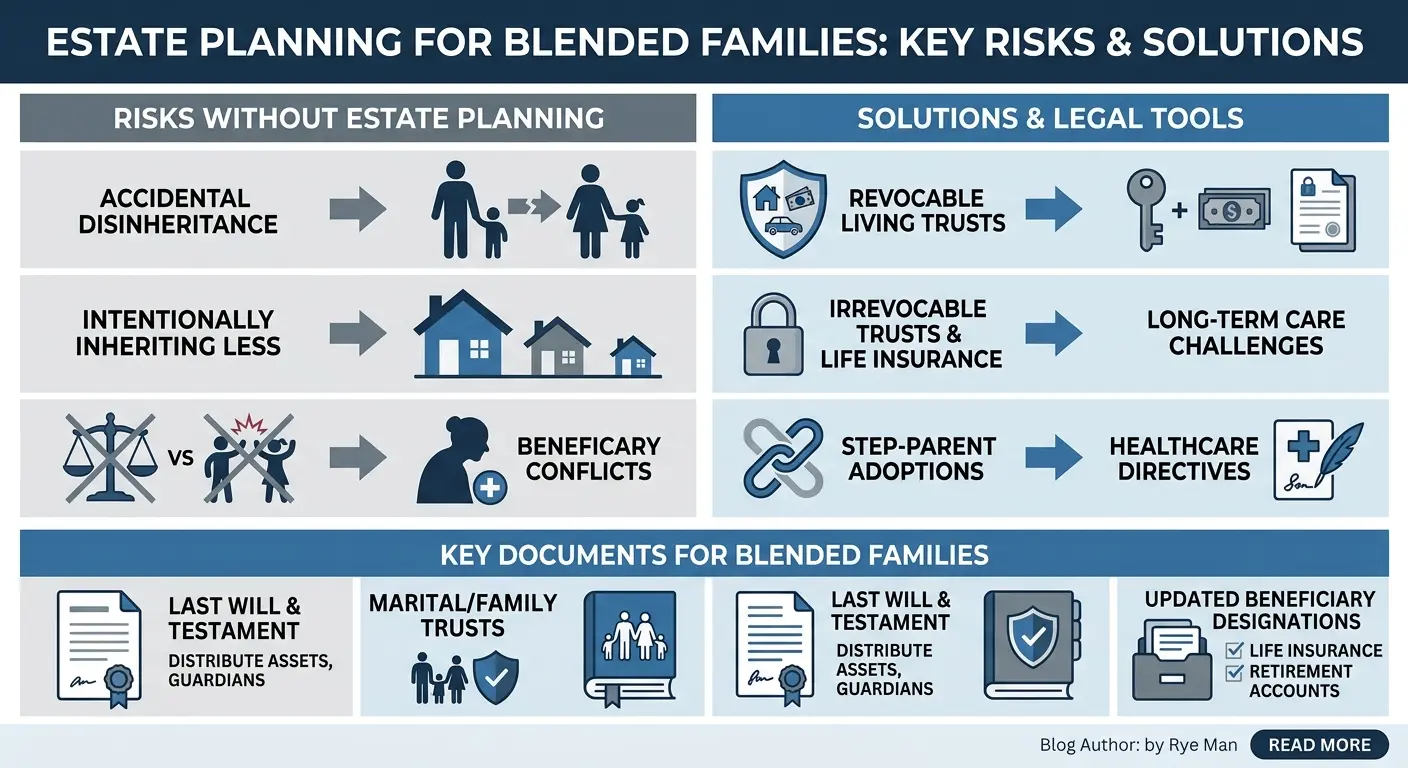

The Essential Documents Every Pennsylvania Blended Family Needs

To bypass default state laws and help ensure your exact wishes are honored, a carefully designed plan must be established. For blended families, this typically involves a combination of legal instruments.

Last Will and Testament

A will is the foundational document of any estate plan. Rather than just hoping for the best, a properly drafted will allow you to:

- Name an executor to manage and settle your affairs.

- Nominate guardians for any minor children.

- Outline exactly how your probate assets should be distributed.

However, a will alone is often not enough to handle the complex dynamics and competing interests of a blended family.

Revocable Living Trust

A revocable living trust is one of the most effective tools for blended families. Its primary benefits include:

- Maintaining control of your assets during your lifetime.

- Specifying exact conditions for how and when assets will be distributed after your death.

- Keeping your family’s finances private, which saves time, can help streamline asset distribution and may help avoid probate for properly titled and funded assets.

Beneficiary Designations

Wills and trusts generally do not control assets with direct beneficiary designations. Coordinating these designations with your overall estate plan is critical for assets such as:

- Retirement accounts (401(k)s, IRAs, pensions)

- Life insurance policies

- Payable-on-death (POD) bank accounts

How to Protect Your Children From a Previous Relationship

Ensuring your children receive their intended inheritance requires specific legal strategies that safeguard assets from future marriages, creditors, or changes in your surviving spouse’s intentions.

Using Trusts to Ring-Fence Your Children’s Inheritance

Rather than leaving assets directly to your children – which could expose the funds to their own financial risks – you can establish specific trusts. These trusts can “ring-fence” certain assets to help ensure they are:

- Managed by a designated trustee whom you trust implicitly.

- Used for your children’s benefit according to your instructions.

- Can offer a level of protection from potential creditors or divorce proceedings, depending on how the trust is structured.

Coordinating With Your Existing Divorce Agreement

Estate planning for a blended family should typically be cross-referenced with your prior divorce decree or marital settlement agreement. Your new estate plan should be designed to comply with prior obligations to prevent your estate from being sued by an ex-spouse. You must generally ensure compliance with:

- Life insurance maintenance stipulations.

- Ongoing child support obligations.

- Alimony or spousal support agreements.

Balancing Your Spouse’s Needs With Your Children’s Inheritance

The ultimate goal for most individuals in a blended family is to provide for their surviving spouse while preserving the intended inheritance for their children.

The QTIP Trust

A Qualified Terminable Interest Property (QTIP) Trust is commonly used in blended family estate planning. Here is how a QTIP trust protects everyone:

- Income for your spouse: The trust generates income to support your surviving spouse for the rest of their life.

- Locked beneficiaries: Your spouse does not have the authority to change the final beneficiaries designated in the trust.

- Helps ensure the remaining assets pass to your intended beneficiaries: Upon your spouse’s passing, the remaining principal is typically distributed to your children.

Life Insurance as an Equalizer

Life insurance can be an excellent tool for dividing an estate fairly without dividing specific assets. This strategy offers several distinct advantages:

- Clear asset division: Your surviving spouse can inherit the family home and retirement accounts.

- Immediate liquidity: Your children receive a substantial, generally income-tax-free death benefit under current federal law directly.

- No co-ownership: It can help prevent your children from having to share ownership of real estate with their stepparent.

Common Mistakes Blended Families Make in Pennsylvania Estate Planning

Navigating estate planning in a blended family requires avoiding several common pitfalls. Be sure to watch out for these frequent errors:

- Relying on joint tenancy: While adding your new spouse to the deed of your home often avoids probate, it generally passes the entire asset to them upon your death, legally cutting out your children from inheriting that property.

- Failing to update documents: Forgetting to revise your estate plan, will, or beneficiary designations after a divorce or remarriage.

- Keeping finances secret: A lack of transparency with your new spouse regarding your financial goals and your obligations to your children.

- Using generic DIY forms: Relying on standard online templates that completely lack the nuance and protective clauses required for complex family dynamics.

Steps to Take Right Now

Protecting your blended family starts with proactive organization. To get started, you should:

- Take a comprehensive inventory of your assets, including real estate, retirement accounts, bank accounts, and life insurance policies.

- Review all current beneficiary designations to help ensure no ex-spouses are still unintentionally listed.

- Have an open, honest conversation with your current spouse about your financial goals and your obligations to your children.

- Gather your prior divorce documents, such as a marital settlement agreement, so your attorney can review compliance.

- Seek qualified legal counsel to formalize your strategy and draft the necessary documents.

How Penglase & Benson Can Help

At Penglase & Benson, we understand that every blended family is unique, and there is no one-size-fits-all solution to estate planning. Balancing the needs of your spouse and your children requires precision, empathy, and a deep understanding of Pennsylvania law.

Our attorneys focus on developing customized legal strategies designed to protect your assets, minimize the risk of family conflict, and help ensure your final wishes are honored. Specifically, we will:

- Review your existing documents and any prior divorce decrees to identify risks.

- Explain your options clearly so you can make informed decisions without the confusing legal jargon.

- Build a comprehensive estate plan that provides peace of mind for you and your loved ones.

Visit our Contact Page to send us a message and schedule your free consultation today.

Frequently Asked Questions

Does my new spouse automatically inherit everything if I die without a will in Pennsylvania?

No. Under Pennsylvania intestacy laws, if you pass away without a will and have children from a previous relationship, the exact distribution depends on your family structure. Typically, your spouse receives an initial statutory amount plus a portion of the remaining estate, and your children divide the rest. Your spouse does not inherit the entire estate, which can lead to complex co-ownership issues.

Can I leave everything to my children and nothing to my spouse?

In Pennsylvania, you generally cannot completely disinherit a surviving spouse unless a valid prenuptial or postnuptial agreement is in place. State law allows a surviving spouse to claim an “elective share,” which typically entitles them to one-third of certain qualifying assets, as defined under Pennsylvania’s elective share rules, regardless of what your will dictates.

What is a QTIP trust, and do I need one?

A Qualified Terminable Interest Property (QTIP) trust is a legal tool that allows you to provide financial support (such as income generated from the trust) to your surviving spouse for the rest of their life. Upon their death, the remaining assets in the trust are distributed to your chosen beneficiaries, usually your children. It is often utilized in blended family planning to help protect both a spouse and children.

What happens to my children from a previous marriage if I die first?

If you die first without a specialized estate plan, any assets you hold jointly with your new spouse will generally pass directly to them, and your children may receive nothing from those assets. Assets held solely in your name will be distributed according to intestacy laws or your will. Protecting your children requires deliberate planning, such as utilizing trusts or life insurance.

How do I protect my spouse without cutting out my kids?

The most effective way to achieve this balance is through customized legal tools. Strategies often include utilizing QTIP trusts, designating specific assets (like life insurance) solely for your children, or clearly dividing assets in a comprehensive living trust to help ensure both your spouse and your children receive their intended inheritance.