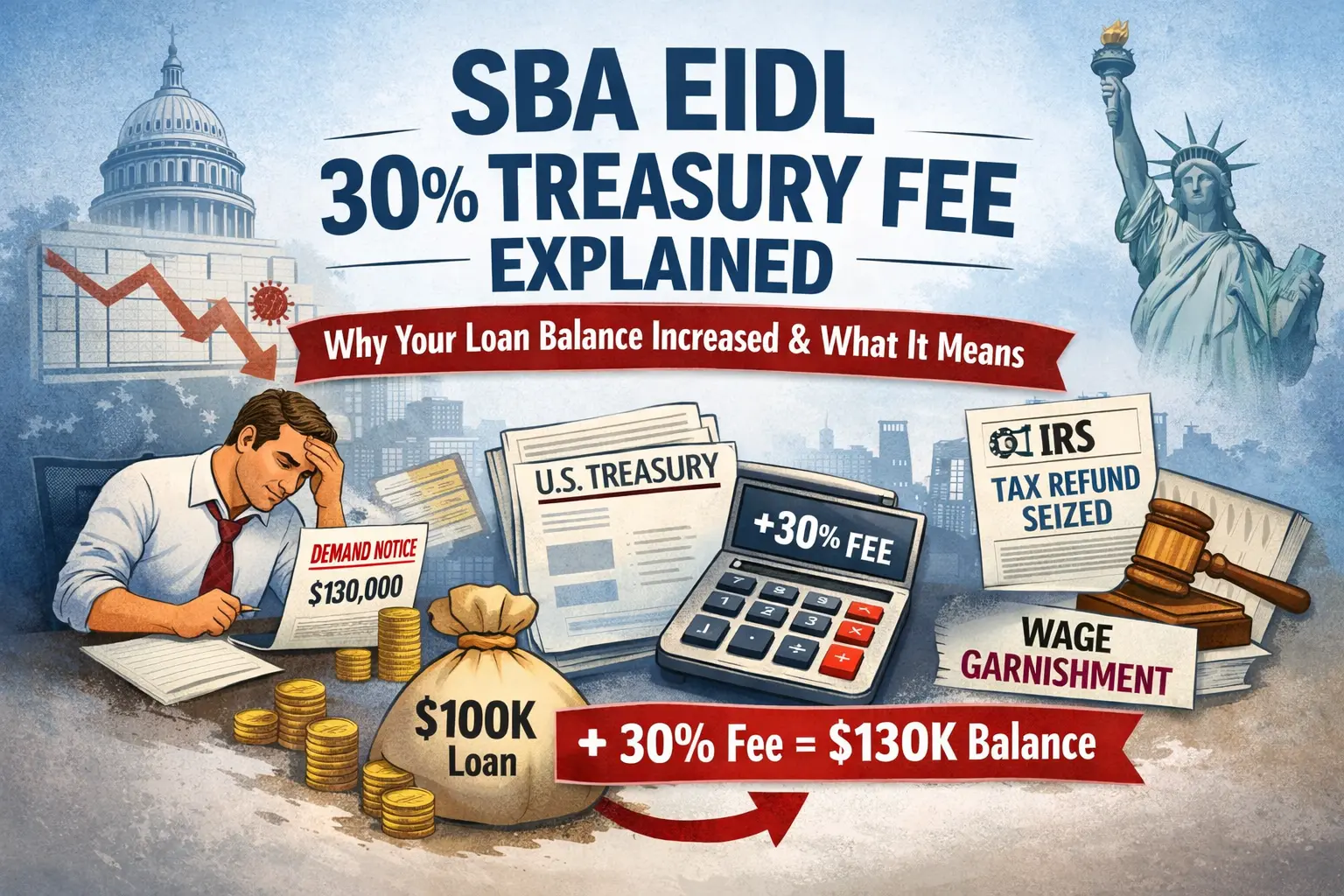

The EIDL Treasury fee is one of the most unexpected financial shocks a small business owner can face. Receiving correspondence from the U.S. Department of the Treasury is stressful enough. For small business owners navigating a defaulted COVID-era SBA Economic Injury Disaster Loan (EIDL), that concern is often compounded upon reviewing the outstanding balance. A business that originally borrowed $100,000 may later receive a demand letter reflecting a balance of $130,000 or more.

This discrepancy is rarely an error. In most cases, it indicates the addition of a Treasury collection fee. This cross-servicing charge often catches business owners off guard, complicating an already difficult financial situation.

If your debt has increased, understanding the mechanics behind this assessment is critical before determining your next steps. The following breakdown explains what this collection fee – often colloquially referred to as the 30% fee – entails, why it is applied to defaulted federal disaster loans, and how it may impact your resolution options moving forward.

The Myth That the Balance You Owe Is Fixed

Many business owners operate under the assumption that a federal loan is a static obligation. You borrow a set amount, it accrues the standard 3.75% interest, and if financial hardship strikes, you simply negotiate a solution based on that original baseline number.

Unfortunately, federal debt collection does not generally work that way. Your EIDL balance is only relatively fixed while it remains in good standing and is serviced directly by the Small Business Administration. Once your loan defaults and is transferred from the SBA, the collection framework changes, and the cost of resolving your debt can increase substantially.

What is the 30% Treasury Collection Fee

When a federal agency refers a defaulted debt for centralized collection, administrative costs are typically passed on to the borrower. Under federal law, specifically the Debt Collection Improvement Act, the U.S. Department of the Treasury is authorized to assess a fee to cover the administrative costs of pursuing the debt.

For SBA EIDL defaults, this federal cross-servicing collection cost can vary depending on circumstances, but is generally in the 28 – 30% range of your outstanding balance. It is important to note what this fee actually entails:

- It is not a fixed statutory percentage.

- It is not a standard late penalty or a new interest rate.

- It represents the federal cross-servicing collection costs added to your debt to fund the government’s collection activities, private debt collectors, and administrative overhead.

Why the Fee Is Added to Your Balance

The federal government operates on the principle that taxpayers should not bear the financial burden of chasing down defaulted loans. Therefore, the cost of collection is generally passed directly onto the borrower.

When the Fee Is Assessed

This collection fee is not applied the moment you miss a single payment. When you first fall behind, your account is considered delinquent, and the SBA attempts to collect the debt internally.

Typically, after approximately 120 days of delinquency, the SBA officially declares the loan in default, accelerates the balance, and transfers your file to the U.S. Department of the Treasury’s Offset Program (TOP) and Cross–Servicing program. It is important to note that the timeline and procedures for Treasury referrals have been subject to policy changes in recent years. If you are uncertain about the current status of your account or when a transfer may occur, consulting with an attorney familiar with current SBA collection practices is strongly recommended. These collection fees are generally assessed upon transfer or shortly following referral to Treasury cross-servicing programs.

How the Fee Compounds With Existing Interest

The calculation of the Treasury fee can make a difficult situation more complex. A cross-servicing collection fee, which can often be in the 28 – 30% range, is generally not calculated merely on your original principal. It is applied to the principal plus whatever interest has already accrued over the years. Because these are typically 30-year loans, the accumulated interest can be considerable. When these cross–servicing costs are added to that combined total, your overall debt liability can increase significantly.

What Changes After the Treasury Fee Is Applied

Once the fee hits your account, it signals a major shift in how your debt is handled. You are no longer dealing with the SBA’s customer service representatives. Your account is typically escalated to the Treasury’s collection apparatus.

The federal government possesses broad collection powers that private creditors generally do not have. Through administrative collection mechanisms, though escalation paths and exact actions may vary, the Treasury may, in many cases:

- Intercept your annual tax refunds.

- Seize certain federal benefits.

- Order your employer to garnish up to 15% of your disposable paycheck.

The addition of these collection fees means administrative wage garnishment and tax refund offsets may be utilized for a longer period to satisfy the increased balance.

How the 30% Fee Affects Your Resolution Options

A notable increase in your debt alters the landscape of how you can resolve the issue.

Treasury Settlement

It is sometimes possible to negotiate a lump–sum settlement with the Treasury, but the increased balance can make this process complex. Because any settlement is calculated based on the new, higher total, a negotiated resolution might still require significant capital.

Settlement amounts vary based on financial hardship and case-specific factors, and resolutions are generally subject to thorough financial disclosure and ability-to-pay evaluations for the government to consider accepting less than the total outstanding balance.

Installment Payment Plans

If you are trying to keep your business open and negotiate a structured payment plan with the Treasury to stop wage garnishment, the fee presents a challenge. Monthly installment agreements are calculated to pay down the total balance over time. A substantially larger balance means your required monthly payment can be proportionately higher, putting even more strain on your cash flow.

Bankruptcy Relief

If you cannot pay the increased debt obligation, bankruptcy remains a viable legal option. The Treasury fee is generally classified alongside the EIDL principal as unsecured debt (for the portion exceeding any collateral value). Depending on your circumstances, relief may include:

- Chapter 7 Bankruptcy: Both the original loan and the collection fees may be dischargeable depending on the case circumstances, subject to eligibility and individual bankruptcy review.

- Chapter 13 or Subchapter V Reorganization: The fee is often lumped into the total debt pool that gets restructured. This means you may pay a fraction of the debt, and the remainder could be addressed at the end of your payment plan, depending on your approved structure.

What the 30% Fee Cannot Change

While these cross-servicing costs significantly increase your total balance, they do not affect your fundamental legal rights. The Treasury process does not affect your right to seek legal counsel, nor does it prevent you from requesting a hearing to challenge a wage garnishment in certain circumstances. Most importantly, the addition of collection fees does not affect your ability to seek protection under the federal bankruptcy code.

Steps to Take If Your Balance Has Already Increased

If you have received a letter showing a substantial balance increase, you may need to act strategically to protect your interests:

- Do not ignore the notices: Ignoring Treasury correspondence can, in certain circumstances, accelerate wage garnishments and tax offsets.

- Do not prematurely agree to a plan: Agreeing to a payment plan you cannot afford just to resolve an immediate collection threat may only set you up for a second default.

- Gather your documents: Locate your original SBA loan authorization and recent tax returns so you have a clear picture of your exposure.

- Consult a law firm: Navigating Treasury cross-servicing can be complex. Legal counsel can evaluate whether a settlement, payment plan, or bankruptcy petition is an appropriate route forward based on your specific circumstances.

How Penglase & Benson Can Help

At Penglase & Benson, we understand the challenges associated with managing a federal obligation that has escalated in cost. You did what you had to do to keep your business alive during a crisis, and you deserve a clear path forward.

Our attorneys focus on finding practical legal strategies for small business owners dealing with SBA loan defaults, Treasury collections, and bankruptcy. When you retain our firm, we represent you in dealings with the U.S. Treasury. Specifically, we:

- Handle communications and correspondence on your behalf.

- Work to address administrative collection actions, such as wage garnishment.

- Develop a roadmap to resolve your outstanding EIDL debt.

If you are facing an SBA EIDL loan default, potential wage garnishment, or complex business debt, Penglase & Benson is available to assist you in exploring your legal options.

Visit our Contact Page to send us a message and schedule your free consultation today.

Frequently Asked Questions

Why did my EIDL balance increase after being sent to Treasury?

Under the Debt Collection Improvement Act, the federal government is authorized to charge borrowers for the administrative costs of collecting defaulted debts. When the SBA transfers your defaulted loan to the Treasury’s Cross–Servicing program, a cross-servicing collection fee, which can vary but is generally in the 28 – 30% range, is typically assessed shortly following referral to Treasury cross–servicing programs and added to your combined principal and accrued interest.

Is the 30% Treasury fee dischargeable in bankruptcy?

Yes. In most situations, the collection fee is treated the same as the underlying EIDL debt. If the EIDL itself is dischargeable in your Chapter 7 or Chapter 13 bankruptcy, the attached Treasury fee may be dischargeable depending on the case circumstances, subject to eligibility and individual bankruptcy review.

Can I dispute or reduce the 30% collection fee?

Disputing the fee itself is rarely successful, as it is authorized by federal statute and tied to federal cross-servicing collection costs. However, you can often address the fee by negotiating a lump-sum settlement on the total overall balance, entering a payment plan, or seeking to discharge the entire debt through bankruptcy.

Does the fee apply even if I’m in a payment plan?

If you establish a payment plan directly with the SBA before the loan defaults and transfers, you may avoid the fee. However, if the loan has already been transferred to the Treasury, the federal cross-servicing collection cost has generally already been applied shortly following referral to Treasury cross-servicing programs, and any Treasury installment plan you negotiate will be based on that higher amount.

What happens to the fee if I settle with Treasury?

If you successfully negotiate a lump-sum settlement with the Treasury, the agreement generally resolves the entire outstanding balance. You pay the agreed-upon settlement figure, and the remainder of the debt – including the collection fees and the unpaid principal – may be forgiven and written off, subject to the specific terms of the settlement agreement and individual case factors.