You closed your business, or perhaps it is barely hanging on, and took a W-2 job to support your family. Then, you open your mail and find a letter from the U.S. Department of the Treasury: a Notice of Intent to Initiate Administrative Wage Garnishment. If you are reading this, you are likely in a state of panic, but while you are not alone, you are on a very strict countdown.

This letter means the federal government is preparing to bypass the court system entirely and take a percentage of your paycheck directly from your employer to satisfy an unpaid Small Business Administration (SBA) Economic Injury Disaster Loan (EIDL). Because this is an EIDL administrative wage garnishment, the Treasury already has the authority to act without suing you, winning a judgment, or asking a local judge for permission.

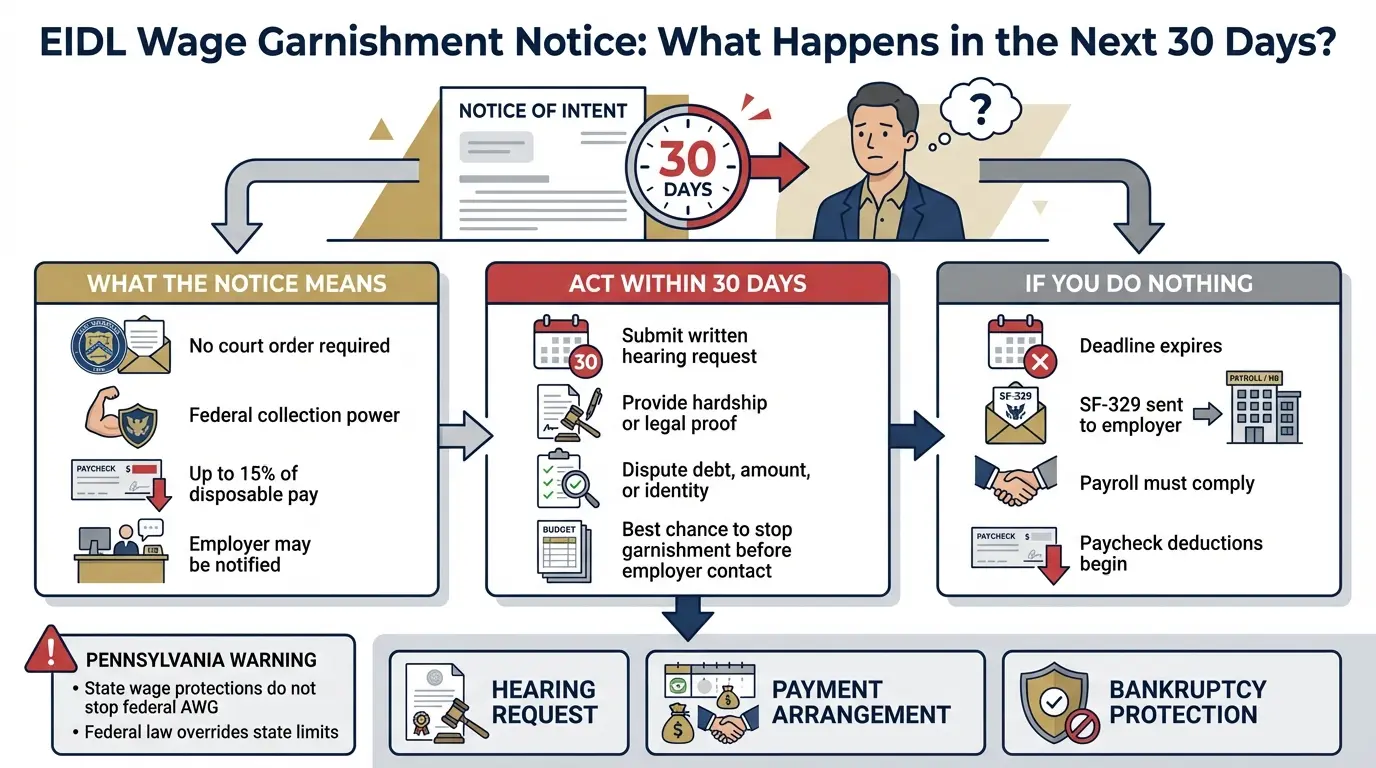

You have exactly 30 days from the date on that letter to take action. This deadline is a hard, legally binding expiration date, and doing nothing guarantees your employer’s HR department will receive an order to start docking your pay. However, you have options; this page explains exactly what this notice means, how the federal garnishment process works, and the steps you must take to protect your livelihood.

What Is an EIDL Administrative Wage Garnishment Notice

An Administrative Wage Garnishment (AWG) is a powerful, federal debt collection tool used by the Bureau of the Fiscal Service (a branch of the U.S. Treasury) to collect delinquent non-tax debts owed to the United States.

To understand the gravity of an SBA EIDL wage garnishment notice, you must understand how it differs from standard debt collection:

| Feature | Private Debt Collection | Federal EIDL AWG |

| Legal Requirement | Must file a lawsuit, win a judgment, and petition the court for an order. | No court order required. The Treasury issues orders directly under the Debt Collection Improvement Act. |

| Garnishment Amount | Varies by state law and judgment. | Up to 15% of your “disposable pay” (gross pay minus mandatory taxes/withholdings). |

| Employer Role | Notified via court-ordered writ of garnishment. | Notified via federal order (SF-329); legally liable for failure to comply. |

| Professional Impact | Involves local court records. | Direct notification to your current HR or Payroll department often causes professional embarrassment. |

The “Notice of Intent” is your final warning before this mechanism is triggered. It outlines the balance owed, the government’s intention to garnish, and your rights to dispute the action, provided you act within the narrow 30-day window.

Why You Received This Notice: How EIDL Debt Reaches Wage Garnishment

Your EIDL account progressed through several distinct collection stages before reaching this point. Because you signed a Personal Guarantee on your loan, you are personally liable for the business debt.

The path: SBA default → Treasury transfer (after 120-180 days) → demand letters and collection calls → AWG authorization after those attempts failed.

For a full breakdown of penalties and fees accumulated along the way, see our guide on EIDL default consequences.

Your 30-Day Window: What the Deadline Actually Means

The date printed on the letterhead, not the postmark, not when you opened it, starts your clock. After 30 days without a formal response, the Treasury mails an SF-329 garnishment order directly to your employer. They are then legally required to begin withholding 15% of your disposable pay within one to two pay periods.

There is no grace period and no secondary appeal once garnishment begins. Stopping it after the fact is significantly harder and more expensive than acting now.

How to Request a Hearing and What Qualifies

To prevent the garnishment order from being sent to your employer, you must submit a written request for a hearing within the 30-day timeframe (often within 15 days if you want a guaranteed stay of the garnishment pending the hearing outcome).

An AWG hearing request EIDL procedure is highly specific. You cannot simply call the Treasury and complain. You must submit a formal written request, provide supporting documentation, and state a valid legal or financial defense.

Valid Reasons for an AWG Hearing

The government will not grant a hearing just because you are unhappy about the debt. You must prove one of the following:

- Financial Hardship: This is the most common defense. You must prove that garnishing 15% of your pay would leave you unable to meet basic, essential living expenses for yourself and your dependents (housing, food, utilities, essential medical care). You will be required to submit a comprehensive financial statement detailing all income, assets, and mandatory expenses.

- Disputed Debt Amount or Validity: You have proof that the balance is incorrect, that the loan was already paid off, or that the debt was legally discharged (e.g., in a prior bankruptcy).

- Identity Error: You did not sign the loan or the personal guarantee, and you are the victim of identity theft.

- Existing Repayment Plan: You have already negotiated and are actively paying on an installment agreement with the Treasury or its collection agency, and they issued the AWG notice in error.

- Recent Involuntary Unemployment: You were involuntarily fired or laid off from a previous job and have been re-employed at your current job for less than 12 months.

Invalid Reasons for a Hearing

The hearing officer will immediately dismiss your request if your defense is:

- “I didn’t know the interest was accumulating.”

- “I thought EIDL loans were going to be forgiven like PPP loans.”

- “The business failed because of COVID mandates, so it’s not my fault.”

- “15% just feels like too much.”

What Happens at the Hearing

Hearings are rarely held in person; they are usually conducted via a review of written records or over a scheduled telephone conference with a hearing official. The official reviews your financial disclosures or legal defenses and makes a binding determination.

It is crucial to understand that simply requesting a hearing does not erase the debt; it is a procedure to determine if the garnishment is legal and financially viable.

Options That Can Actually Stop Wage Garnishment

If you have received an AWG notice, you are looking for how to stop EIDL wage garnishment permanently, or at least manageably. There are realistically three avenues:

- Bankruptcy (Automatic Stay): Filing Chapter 7 or Chapter 13 immediately triggers a federal injunction that legally halts all Treasury collection activity, including active garnishments.

- Negotiated Payment Arrangement: If Treasury or its collection agency still holds your account, a voluntary installment agreement can suspend AWG action. This requires swift negotiation before the 30-day window closes.

- Settlement / Offer in Compromise: A lump–sum settlement for less than the full balance is theoretically possible but requires documented, severe, and permanent financial hardship.

What Pennsylvania Borrowers Need to Know

If you are a business owner living in Doylestown, Bucks County, Montgomery County, or anywhere else in Pennsylvania, you face a unique and dangerous legal reality regarding federal wage garnishment.

Pennsylvania state law is famously protective of debtors. Under standard PA law, wage garnishment is strictly prohibited for almost all consumer and commercial debts (with narrow exceptions for things like child support, back rent, or student loans). Many PA residents falsely believe that their wages are completely safe from creditors.

This protection does not apply to SBA EIDL loans.

Because an AWG is a federal collection mechanism, the Supremacy Clause of the U.S. Constitution dictates that federal law preempts state law. The Treasury absolutely can, and will, garnish the wages of Pennsylvania residents, completely bypassing PA’s state-level wage protections.

Furthermore, Pennsylvania homeowners face another vulnerability regarding the protection of their property. Unlike many states with robust homestead exemptions that shield significant home equity from creditors, Pennsylvania’s statutory protections for a debtor’s residence are shockingly low and offer almost no defense against a federal judgment lien.

For a homeowner in Bucks County with significant equity in their house, a federal judgment resulting from an EIDL default can easily threaten their real estate. This massive disparity between state illusions of safety and harsh federal reality is exactly why consulting with a local Pennsylvania attorney who understands federal SBA debt is critical.

Steps to Take If You Received an AWG Notice

If you are holding a Notice of Intent to Initiate Administrative Wage Garnishment, time is your most valuable asset. Follow this checklist immediately:

- Check the date printed on the Treasury letterhead – that is day one of your countdown.

- Count 30 calendar days forward and mark the hard deadline.

- Locate your original EIDL closing documents and confirm whether your name appears on the Personal Guarantee.

- Identify who sent the notice – the Bureau of the Fiscal Service directly, or a Private Collection Agency acting on their behalf.

- Do not ignore it. Inaction guarantees your employer receives the garnishment order.

- Do not call without a plan. Panicked calls can backfire – avoid volunteering your employer’s name or making payment commitments you cannot keep.

- Consult a qualified attorney before the deadline.

If you’re unsure how your account ended up there, our guide on Treasury referrals explains the full transition.

How Penglase & Benson Can Help

At Penglase & Benson, we understand the immense stress caused by a federal wage garnishment notice. You did not transition to a W-2 job only to have the government seize your earnings. Our attorneys are dedicated to helping individuals navigate the Treasury collection process. We focus on finding the right strategy to stop or manage your AWG, without judgment.

When you hire our firm, we step between you and the U.S. Treasury. Here is what we do for you:

- Handle all communications and phone calls from Treasury collectors and private agencies.

- Scrutinize the AWG notice and process for any procedural errors or legal violations.

- Halt immediate garnishment actions by preparing formal hearing requests and proving financial hardship.

- Build a comprehensive roadmap to resolve your EIDL debt via installment plans, settlements, or bankruptcy protection.

Receiving a Notice of Intent to Initiate Administrative Wage Garnishment is frightening. However, living in fear guarantees that your paycheck will be targeted. You have fundamental legal rights to dispute a garnishment. You simply need to take the first step and ask for legal help.

Don’t let the U.S. Treasury dictate your financial future or compromise your standing with your employer. If you are struggling with an EIDL wage garnishment notice, Penglase & Benson is here to protect you.

Visit our Contact Page to send us a message and schedule your free consultation today.

Frequently Asked Questions (FAQ)

Can the government garnish my wages for an EIDL loan without suing me?

Yes. Under the Debt Collection Improvement Act, the federal government does not need to file a lawsuit or obtain a court judgment to garnish your wages for federal non-tax debts like an SBA EIDL. They use an Administrative Wage Garnishment (AWG) order, which is issued directly to your employer.

How much of my paycheck can the Treasury take?

The Treasury can legally garnish up to 15% of your disposable pay. Disposable pay is calculated as your gross income minus legally mandated deductions like taxes and Medicare. It does not subtract your voluntary deductions like 401(k) contributions or private health insurance, meaning the actual impact on your take-home cash is usually severe.

What happens if I ignore the AWG notice?

If you ignore the notice and let the 30-day window expire, you waive your right to a pre-garnishment hearing. The Treasury will automatically mail an SF-329 garnishment order to your employer’s payroll department, and they will be legally required to begin deducting 15% of your pay within one to two pay cycles.

Can I stop wage garnishment by filing for bankruptcy?

Yes. Filing for federal bankruptcy (Chapter 7 or Chapter 13) immediately enacts the “Automatic Stay.” This is a federal injunction that legally forces all creditors, including the U.S. Treasury, to immediately halt all collection efforts, including active or pending wage garnishments.

Does Pennsylvania law protect me from federal wage garnishment?

No. While Pennsylvania state law heavily restricts wage garnishment for standard consumer debts, an EIDL default is a federal debt. Federal law preempts state law, meaning the U.S. Treasury can absolutely garnish the wages of Pennsylvania residents, regardless of state-level protections.

How do I request a hardship hearing for EIDL wage garnishment?

You must submit a formal, written request for a hearing within 30 days of the notice date. To claim financial hardship, you must provide comprehensive documentation proving that the 15% deduction would render you unable to pay for necessities (housing, food, utilities). The forms and evidence required are extensive and must be filed exactly as instructed in your notice.