Six years after the pandemic shutdowns, many business owners are still dealing with the fallout of emergency borrowing. EIDL funds once provided short-term relief, but for many borrowers, that relief has turned into a serious long-term debt burden.

For some businesses, revenue never fully recovered enough to cover both normal operating costs and large federal loan payments. As balances grow and collection notices escalate, many owners realize the business cannot generate enough cash flow to catch up.

That financial pressure often creates fear about personal assets, professional stability, and family security. Although the federal government has strong collection powers, bankruptcy law can provide a legal path to address and sometimes eliminate qualifying SBA debt.

The Myth That Federal Loans Are Bankruptcy-Proof

A widespread misconception dictates that you cannot eliminate money owed to the federal government. Many borrowers confuse an EIDL loan with non-dischargeable obligations like student loans or specific federal tax debts. This misunderstanding prevents business owners from seeking the legal protection they desperately need.

In reality, an SBA EIDL loan is generally treated as a standard commercial obligation under the federal bankruptcy code. The debt is subject to the jurisdiction of the bankruptcy court. A properly filed and executed bankruptcy case may result in a discharge of the remaining balance, depending on the facts and subject to certain exceptions like fraud or misrepresentation.

What Type of Debt Is an EIDL Loan in Bankruptcy

The bankruptcy court categorizes your debt based on the size of the loan and the specific documents you signed. Understanding your exact liability requires looking at two distinct thresholds:

- Loans exceeding $25,000: The SBA required collateral for these amounts, creating a secured debt backed by a UCC-1 lien on your business assets.

- Loans exceeding $200,000: The SBA required an unconditional personal guarantee from every owner holding 20% or more ownership interest in the business.

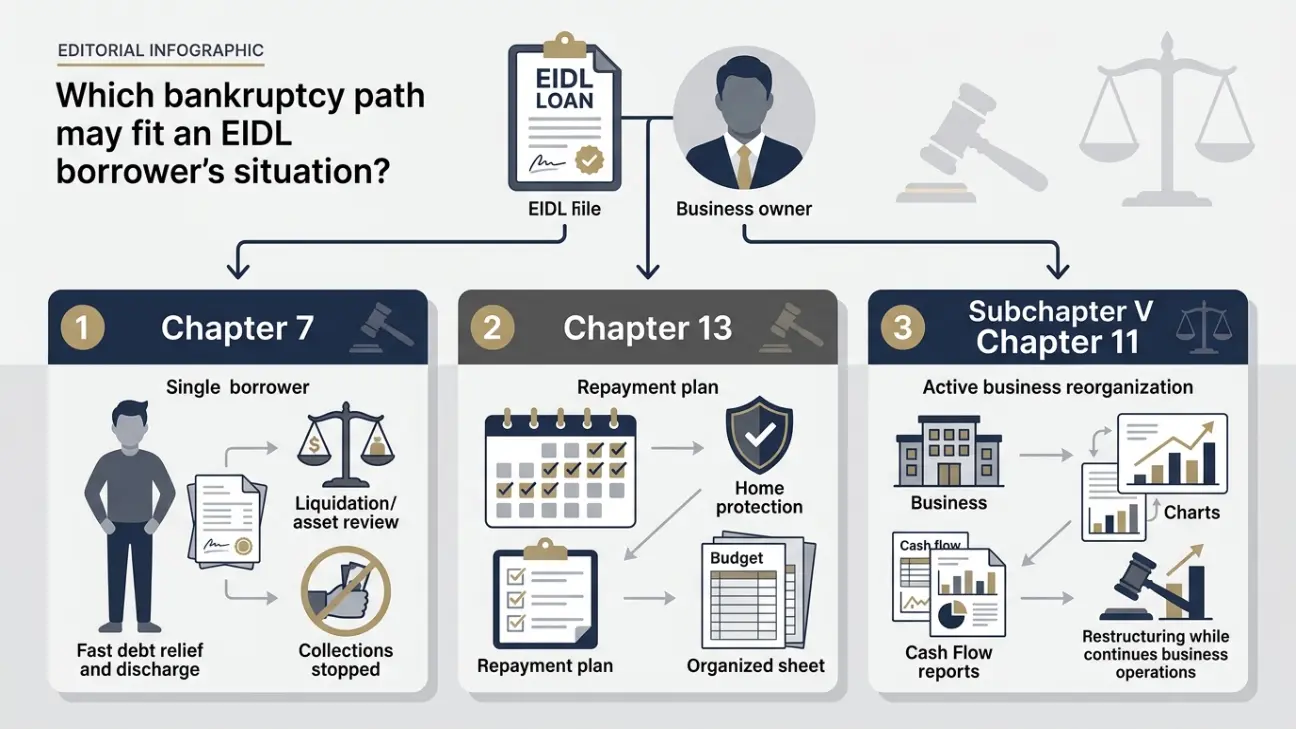

Chapter 7 Bankruptcy and EIDL Debt

Chapter 7 bankruptcy is a liquidation process, but its effects vary drastically depending on who is filing. For individual business owners, it is designed to quickly wipe out qualifying personal debts.

For business entities like corporations or LLCs, it provides an organized liquidation framework but does not grant a legal discharge of the entity’s debt. The process requires a thorough evaluation of your income and assets before the court grants relief.

Who Qualifies for Chapter 7

Not every individual borrower is eligible to file for this specific chapter. The court applies a strict means test to evaluate your current financial situation by examining several key qualifying factors:

- Income comparison: This test compares your household income to the state median income.

- Household size: The court specifically factors in the size of your family when evaluating these limits.

- Disposable income threshold: The test calculates whether you have sufficient disposable income remaining after allowable expenses.

- Exceeding the limit: If your income exceeds the threshold and you have disposable income, the court may require you to repay a portion of the debt under a different chapter.

What Happens to Your Personal Liability

A successful filing generally results in the discharge of your personal liability for the EIDL loan. The moment your case is filed, an automatic stay goes into effect to halt collection activity in several specific ways:

- Stopping Treasury Cross-Servicing: This federal injunction generally stops most ongoing Treasury Cross-Servicing collection efforts.

- Halting Administrative Wage Garnishment: The stay usually blocks the government from initiating or continuing Administrative Wage Garnishment against your paycheck.

- Future tax offsets: Filing usually stops future tax offsets, although refund and setoff rights may still require case-specific review.

- Meaning of discharge: A discharge legally forbids the creditor from ever demanding payment from you personally for the discharged debt, subject to certain legal exceptions.

What Chapter 7 Cannot Protect

The bankruptcy code does not strip away valid, pre-existing liens on physical collateral. The court generally eliminates your in personam liability (your personal duty to pay) but leaves the following exposures intact:

- Valid UCC-1 liens: The government can still theoretically repossess pledged business assets to satisfy the in rem liability.

- Non-exempt property: The bankruptcy trustee holds the power to liquidate valuable personal assets that fall outside your state’s exemption limits.

This means the physical property of the business remains exposed, even though the government cannot pursue your personal bank accounts for the remaining unsecured deficiency.

Chapter 13 Bankruptcy and EIDL Debt

Chapter 13 is a reorganization process designed for individuals with a regular income. This path allows individual borrowers to protect valuable personal assets while paying back a portion of what they owe. It provides a highly structured legal environment to resolve federal debt and manage personal guarantee exposure without the immediate threat of asset seizure.

How the Repayment Plan Works

The bankruptcy court relies on a structured approach to resolve your debts over time. This process involves four specific elements regarding your repayment plan:

- Plan duration: The court approves a repayment plan that lasts between three and five years.

- EIDL classification: Your EIDL loan is typically treated as a general unsecured claim within this plan, provided the business collateral is no longer an issue or has been properly addressed.

- Payment distribution: The SBA must generally compete with your other unsecured creditors for a pro-rata share of your monthly plan payments.

- Monthly amount calculation: You pay what you can afford based on a strict court-approved budget, rather than the total amount owed.

Protecting Your Home With Chapter 13

Borrowers who signed a personal guarantee often live in constant fear of the government placing a lien on their primary residence. The automatic stay generally prevents creditors from initiating lawsuits or recording property liens against your home.

Furthermore, state homestead exemption laws can work alongside the repayment plan to help ensure you do not lose your house, though the outcome depends on your existing equity, state exemptions, and any current property liens.

What Happens to the Remaining EIDL Balance

You only pay the required monthly amount during the three to five years of your active plan. Once you complete the final payment and all plan requirements, the court generally issues a permanent discharge for the remaining eligible balance. You can walk away free of the remaining dischargeable debt and safe from future collections.

Chapter 11 Subchapter V for Still-Operating Businesses

Congress created Subchapter V to give small business owners a streamlined and cost-effective way to restructure their debts. This chapter allows eligible businesses to retain assets and renegotiate obligations without the massive expense of a traditional corporate bankruptcy. It is an incredibly powerful tool for companies struggling with federal relief loans.

Who Subchapter V Is Designed For

The fundamental goal of this chapter is to save the enterprise and preserve jobs while adjusting the debt load. To qualify for Subchapter V, a business must meet specific eligibility requirements:

- Business operation: This chapter is designed primarily for businesses that maintain commercial operations, depending on the Bankruptcy Code.

- Revenue generation requirement: The enterprise must be engaged in commercial or business activities on the petition date

- Debt limit threshold: As of 2026, total noncontingent liquidated debts cannot exceed $3,424,000, and at least 50% must come from business activities.

- Debt structure: Eligibility also depends heavily on how your specific debt is structured and whether the majority of it arose from commercial activities.

How It Reduces the EIDL Principal

This process utilizes a legal mechanism known as a cram-down to potentially reduce the secured portion of your EIDL loan. The court may tie the secured value of the loan to the current fair market value of your actual business collateral.

The remaining unsecured balance is treated differently under the reorganization plan and may be discharged upon successful completion of the court-approved requirements.

How Bankruptcy Compares to Settlement and Payment Plans

Borrowers facing default on a federal loan have several potential paths forward. Choosing the wrong strategy can cost you significant time, drain your remaining cash, and leave your personal assets exposed. The table below compares the primary resolution methods available.

| Resolution Option | Stops Garnishment Immediately | Eliminates Full Balance | Requires a lump sum | Credit Impact | Best For |

| Treasury Settlement | No | No (partial discount only) | Yes | Serious | Borrowers with cash reserves |

| Installment Payment Plan | Partial | No | No | Serious | Businesses with steady cash flow |

| Chapter 7 Bankruptcy | Yes (automatic stay) | Generally (individual personal liability) | No | Serious (reporting varies) | Overwhelming debt, eligible individuals |

| Chapter 13 Bankruptcy | Yes (automatic stay) | Generally (after plan completion) | No | Serious (reporting varies) | Employed individuals protecting assets |

| Subchapter V (Ch. 11) | Yes (automatic stay) | Partially (based on plan) | No | Serious (reporting varies) | Eligible small businesses reorganizing |

The right resolution depends on your specific financial situation. Bankruptcy provides the strongest immediate protection through the automatic stay, but every option carries trade-offs that require careful evaluation.

What Bankruptcy Cannot Do for Your EIDL Loan?

Transparency regarding the limitations of the bankruptcy court is critical for your financial planning. The court provides immense relief, but it does not offer blanket immunity for every situation. Specifically, filing a petition will not protect you from the following issues:

- Fraud liability: Bankruptcy does not eliminate criminal or civil liability tied to fraud, false statements, or misuse of loan proceeds.

- Fraudulent conveyance claims: The court will not protect improper transfers of business assets or cash made to family members shortly before filing.

- Co-signer obligations: The process does not eliminate the separate legal obligation of a business partner or spouse who also signed a personal guarantee.

Filing for bankruptcy with the explicit intent to hide assets or defraud the government is a serious federal offense that will not be protected by the court.

Steps to Take Before Filing Bankruptcy on an EIDL Loan

Preparation dictates the success of any legal strategy involving federal debt. Before taking formal action, you must gather facts and secure your documentation.

- Locate and review the original EIDL loan authorization: You must read the specific terms you agreed to rather than relying on memory.

- Determine if a personal guarantee was signed: Check the closing documents to see if you accepted personal liability for the corporate debt.

- Identify any UCC-1 lien filings against business assets: Search state records to confirm exactly what property the government claims as collateral.

- Gather recent tax returns, P&L statements, and bank statements: Financial transparency is a strict requirement for filing any bankruptcy petition.

- Stop transferring assets or making unusual payments: Moving money or equipment right before filing creates a severe risk of a fraudulent conveyance investigation.

- Consult a bankruptcy attorney before contacting Treasury or collection agencies: Speaking to collectors without counsel can result in damaging admissions or flawed agreements.

- Do not make verbal commitments to collectors about repayment: Unenforceable promises only complicate your legal standing and delay proper resolution.

How Penglase & Benson Can Help

Penglase & Benson provides focused legal counsel to business owners facing SBA EIDL defaults and other federal debt matters. If your loan has been referred to Treasury Cross-Servicing or you are dealing with collection pressure, we help you assess your situation clearly and respond strategically.

We can assist you by:

- Reviewing your loan documents and related records.

- Assessing your exposure under the personal guaranty and collateral rules.

- Identifying realistic options based on your financial situation.

- Organizing the documents needed for a dispute, hardship request, settlement, or bankruptcy review.

- Communicating with Treasury or private collection agencies on your behalf.

Our goal is to help you understand your exposure, avoid costly mistakes, and choose a response strategy grounded in the facts. If you are facing an SBA EIDL default, wage garnishment, or overwhelming business debt, Penglase & Benson is here to help.

Visit our Contact Page to send us a message and schedule your free consultation today.

Frequently Asked Questions

Can I file bankruptcy on a federal government loan?

Yes. SBA disaster loans are generally eligible for bankruptcy treatment and are usually handled like commercial debt, though the outcome depends on whether the debt is secured and whether any legal exceptions apply.

Will bankruptcy immediately stop wage garnishment?

Generally, yes. Filing usually triggers the automatic stay, which stops most collection activity, including ongoing or threatened wage garnishment in many cases.

Does bankruptcy eliminate the Treasury collection fee added to my balance?

In many cases, yes. If the debt is dischargeable, bankruptcy can generally eliminate the remaining eligible balance, including interest and collection-related charges.

Can I keep my business open after filing for bankruptcy?

It depends on the chapter and your business structure. Chapter 7 often leads to liquidation, while Subchapter V may allow an eligible business to keep operating and restructure its debts.

Is it too late to file for bankruptcy if my EIDL is already at Treasury?

Generally, no. Even after a Treasury referral, filing bankruptcy can still halt collection activity and bring the matter under bankruptcy court protection.