For many small business owners, a COVID EIDL loan has transitioned from a temporary lifeline into a serious collection risk. Your business may have closed, revenue may have fallen short, and you may now be facing federal collection pressure for a balance you cannot repay. In this stressful environment, searching for a way to settle the debt often leads borrowers to consider an SBA Offer in Compromise (OIC) as a potential exit strategy.

However, treating an OIC as a simple or guaranteed solution is a dangerous mistake. While an SBA settlement mechanism exists, the reality for borrowers in 2026 is that the eligibility rules are strict, and submitting the wrong documentation can expose your remaining assets. Pursuing an unrealistic settlement strategy often wastes critical time while your loan balance grows and federal collection risks escalate.

Before you fill out a single form, you must understand exactly what you are facing. This guide explains what an SBA Offer in Compromise is, why confirmed approvals remain rare, the specific financial documents required, how to calculate a realistic offer, the potential tax consequences, and alternative strategies that might better protect your financial future.

What Is an SBA Offer in Compromise

An SBA Offer in Compromise is a formal request submitted by a borrower asking the government to accept a partial lump-sum payment to satisfy the full balance of a defaulted loan. It is vital to understand that an OIC is a negotiated settlement, not loan forgiveness.

When you submit an OIC, the government evaluates whether accepting your settlement offer will recover more money than pursuing continued collection actions. The process involves complete financial disclosure, requiring you to document your inability to pay the debt in full. It is a request for a compromise, not a guaranteed right, and the SBA holds strict standards for approval.

The Reality in 2026: OIC for COVID EIDL Loans Is Rarely Approved

If you search for advice online, you will likely find discussions presenting an SBA Offer in Compromise as a routine, straightforward way to cut your debt in half. For borrowers dealing with COVID EIDL loans in 2026, this narrative is highly misleading.

In practice, confirmed approvals for COVID EIDL compromises appear extremely rare. The SBA does not treat an OIC as a simple request for a discount; it reviews your hardship, remaining assets, business status, and the amount the government could realistically recover through collection. Submitting the paperwork does not mean you have a strong case. Approval is difficult, highly fact-specific, and never guaranteed.

The Conditions That Must Be Met Before You Can Apply

Eligibility for an OIC is not based simply on a borrower’s desire to lower their balance. The government imposes strict prerequisites that must be satisfied before it will seriously review a settlement package.

- Loan status: The loan must generally be in default or in liquidation. The SBA rarely considers compromising loans that are current or merely delinquent without formal acceleration.

- Business closure: The SBA typically requires the business entity associated with the loan to be permanently closed or to demonstrate a severe inability to continue operations.

- Collateral liquidation: For loans over $25,000, pledged business assets generally must be sold, with the proceeds applied to the loan balance before a compromise is considered.

- Complete financial disclosure: You must provide comprehensive personal and business financial records, including all accounts, income, and assets.

- No fraud or misuse: Evidence that you misused EIDL funds or committed application fraud will typically disqualify you from a settlement.

- Reasonable offer amount: The lump-sum offer must reflect a realistic recovery value for the government relative to the cost of forced collection.

When OIC Makes Sense and When It Does Not

Deciding whether to submit an Offer in Compromise requires an objective look at your financial reality. Because the application exposes your current financials, applying when you are clearly ineligible can be counterproductive.

| Scenario | OIC May Make Sense | OIC Likely Does Not Make Sense |

| Business Status | The business is legally dissolved and closed, with zero ongoing revenue. | The business is still operating, generating cash flow, or paying other creditors. |

| Business Assets | All assets have been legally liquidated, and the funds have been applied to the SBA loan. | Assets were transferred to a new company, sold to family, or are unaccounted for. |

| Financial Hardship | The guarantor has minimal equity, negligible savings, and documented financial hardship. | The guarantor has substantial home equity, high income, or hidden investment accounts. |

| Collection Stage | The loan is accelerated but still actively managed by the SBA liquidation team. | The debt is already subject to active Treasury referral collection measures. |

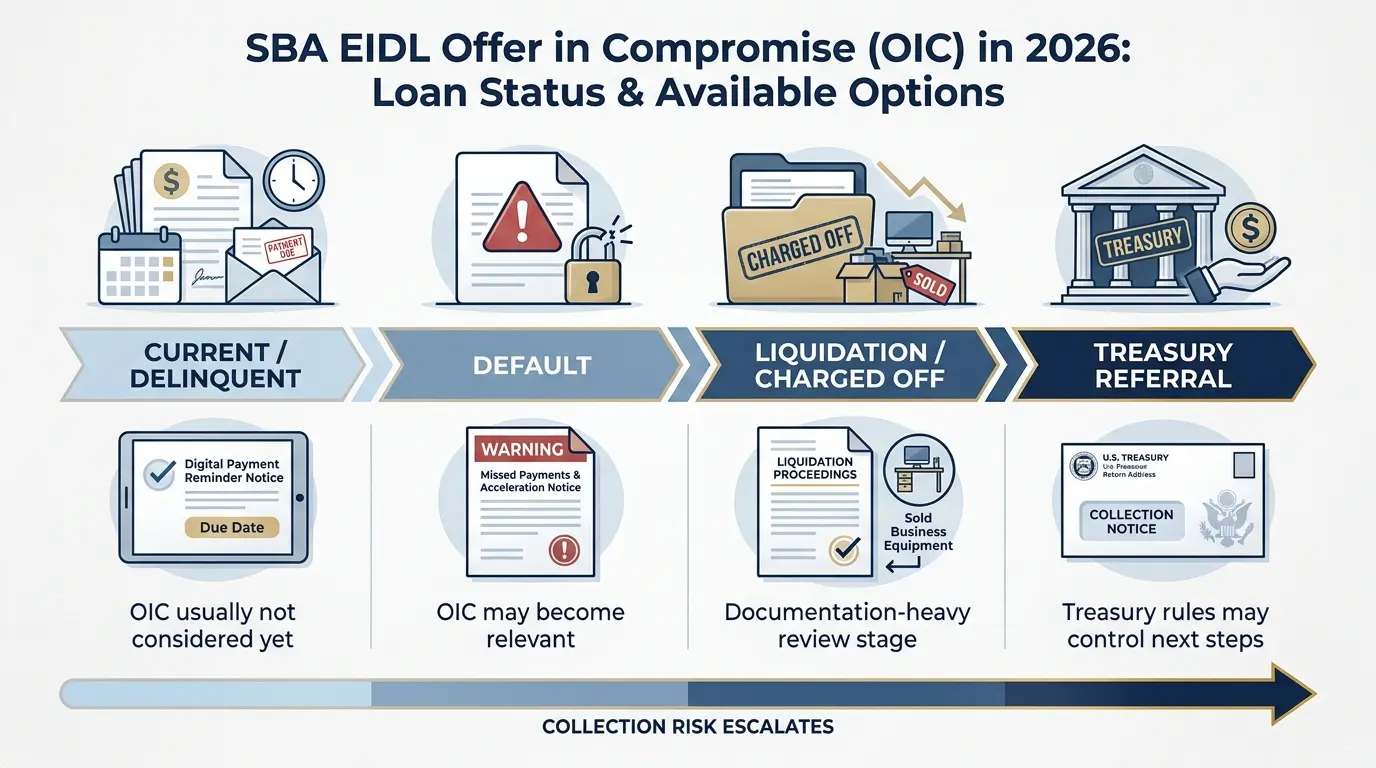

Why Your Loan Status Determines What Is Still Possible

The timeline of your debt heavily dictates your available options. The same borrower will face different procedural rules depending on whether the SBA still controls the loan or if the debt has been escalated.

| Loan Status | What It Means | Why It Matters for OIC or Settlement |

| Current / Delinquent | Payments are up to date or have been missed only recently. | The SBA generally will not entertain an OIC. You are expected to resume payments or request a hardship accommodation. |

| Default | The SBA has accelerated the loan due to missed payments. | Serious EIDL loan default consequences begin, and the SBA’s liquidation team may consider a formal OIC package. |

| Liquidation / Charged Off | The SBA has moved the loan into a recovery or liquidation stage. | This is often where an OIC becomes more procedurally relevant, but approval remains difficult and never guaranteed. |

| Treasury Referral | The SBA has transferred your debt to the U.S. Treasury. | The SBA may no longer be the primary contact, and Treasury referral rules may control the next stage. The standard SBA OIC path may no longer be the right process. |

What Documents the SBA Requires in a Complete OIC Package

The OIC process is heavily document-driven. The SBA will not take your word that you are facing financial hardship; they require sworn, documented proof. Submitting weak or inconsistent documentation damages your credibility.

The Core Forms: SBA Form 1150 and SBA Form 770

A complete package revolves around two highly detailed federal documents. SBA Form 1150 is the actual Offer in Compromise document, stating the exact lump-sum amount you are offering and the source of the funds.

SBA Form 770 is the Financial Statement of Debtor. This form requires a detailed breakdown of your personal assets, liabilities, monthly income, and living expenses to demonstrate your ability or inability to pay. Inconsistencies between these forms and your actual bank records will undermine your application.

Supporting Financial Documents the SBA Will Review

To verify the claims made on your forms, the SBA typically requires supporting evidence to prove your financial standing:

- Bank statements: Prove your current cash flow, spending habits, and account balances.

- Tax returns: Verifies your historical income and business revenue.

- IRS Form 4506-C: Allows the SBA to verify your tax return information directly with the IRS.

- Pay stubs or income records: Establishes your current earning capacity and employment status.

- Collateral records: Shows that pledged business inventory and equipment were properly liquidated at fair market value.

- Proof of business closure: Evidence showing the business has stopped operating, formally dissolved, canceled licenses, or otherwise ceased activity.

- Real estate information: Determines if you have available home equity that could be tapped to pay the debt.

How to Calculate What You Should Actually Offer

One of the most common mistakes borrowers make is offering a random amount based purely on what they wish to pay, rather than what the government could legally collect from them. Lowball offers usually fail because the SBA evaluates whether forced collection yields a higher return than your proposed lump sum.

Your offer must be rooted in the realistic recovery value of your account. Factors that can affect your offer amount include:

- Available cash: Liquid savings and cash on hand.

- Recoverable assets: Home equity or other personal property.

- Current income: Your ongoing earning ability and employment status.

- Personal guarantee exposure: Liability attached to individual guarantors.

- Collateral recovery: The remaining value of pledged business assets.

- Third-party funds: Access to a gift or loan from a family member.

- Guarantor strength: The financial situation of each person who signed the loan.

If the SBA determines they could recover more over time, a low offer will likely be rejected. Additionally, if an offer is accepted, borrowers must typically be prepared to wire the funds within a strict deadline, often 30 to 60 days.

The Tax Trap Most Borrowers Never See Coming

Even if the SBA approves your settlement, the forgiven balance may create a separate tax issue known as cancellation of debt income.

Under IRS rules, debt canceled through a settlement can sometimes be treated as taxable income. For example, if you owe $150,000 and the SBA accepts $50,000, the remaining $100,000 may be treated as canceled debt, even though you never received that amount in cash.

However, exceptions may apply. Before finalizing any settlement, review these issues with a qualified tax professional:

- Whether the canceled balance could create a tax liability.

- Whether the insolvency or bankruptcy exclusions may apply.

- Whether IRS Form 982 may be needed to claim an exclusion for canceled debt.

What Happens After You Submit Your OIC

Submitting an OIC package is the beginning of a lengthy review phase. The SBA liquidation team will review the file, request clarification, and eventually issue a formal decision.

If the SBA Approves Your Offer

If your offer is accepted, you should not assume the matter is fully resolved until the written terms are reviewed carefully. You must confirm the exact payment deadline and the required transfer method, along with written confirmation of the release terms.

It is critical to verify explicit release from any personal guarantee, the process for releasing UCC liens filed against business property, whether the settlement covers all guarantors or only the individual who submitted the offer, and any potential tax reporting issues.

If the SBA Rejects Your Offer

If your offer is rejected, it generally means the SBA believes alternative collection methods or a payment plan could recover more money. Federal collection pressure may resume or escalate, and the balance may be subject to the 30% Treasury collection fee if the debt is transferred. You cannot afford to ignore notices after a rejection; you must evaluate payment plans or other legal strategies immediately.

Other Paths if OIC Is Not the Right Option for You

If an SBA Offer in Compromise is not realistic for your situation, other legal or repayment strategies may still be available to protect your assets. Depending on your specific financial exposure, you may need to consider:

- Treasury payment arrangements

- SBA hardship programs

- Responding to collection notices

- Bankruptcy review

How Penglase & Benson Can Help

Navigating an EIDL loan default requires a precise, legally sound strategy. Submitting a poorly prepared OIC can create avoidable mistakes, weaken your negotiating position, or cause you to miss better alternatives. Penglase & Benson provides focused legal counsel to business owners facing federal debt.

We protect our clients by taking concrete actions:

- Reviewing loan status: Determining if the debt is actively managed by the SBA or if it has escalated to the U.S. Treasury.

- Assessing exposure: Evaluating your personal guarantee, collateral, and UCC lien risks.

- Evaluating OIC viability: Formulating a realistic offer strategy before you submit weak documentation.

- Preparing documentation: Reviewing complex financial records to ensure accuracy and legal compliance.

- Identifying alternatives: Exploring protective legal strategies and potential tax risks if settlement is not the best path.

Do not wait for federal collection efforts to escalate.

Visit our Contact Page to send us a message and schedule your free consultation today.

Frequently Asked Questions

Will applying for an OIC automatically stop collections?

No. Submitting an application does not guarantee a pause on collections or Treasury offsets. The government may continue to pursue recovery while your offer is under review.

Are multiple guarantors reviewed separately?

Yes. The SBA evaluates each guarantor’s financial strength separately. They may focus collection efforts on guarantors with stronger recoverable assets rather than accepting a low settlement.

Can I still negotiate if my EIDL loan is already with Treasury?

Once your debt is referred to Treasury, the standard SBA Form 1150 process may no longer apply. Please refer to our guide on Treasury referral for full details.

Can a rejected OIC create additional risk?

Yes. Submitting comprehensive financial records provides the government with an updated view of your bank accounts, income streams, and assets. This information could be used to direct future collection efforts if the offer is denied.

Should I use retirement funds to make a lump-sum offer?

Retirement accounts often have specific legal protections against debt collection. You should not liquidate protected assets to pay an unprotected debt without first consulting qualified legal and tax professionals.

Do I need an attorney, a CPA, or both?

An attorney is critical for evaluating personal liability, assessing collection risks, and developing a protective legal strategy. A CPA is highly recommended to address the complex tax consequences associated with canceled debt.