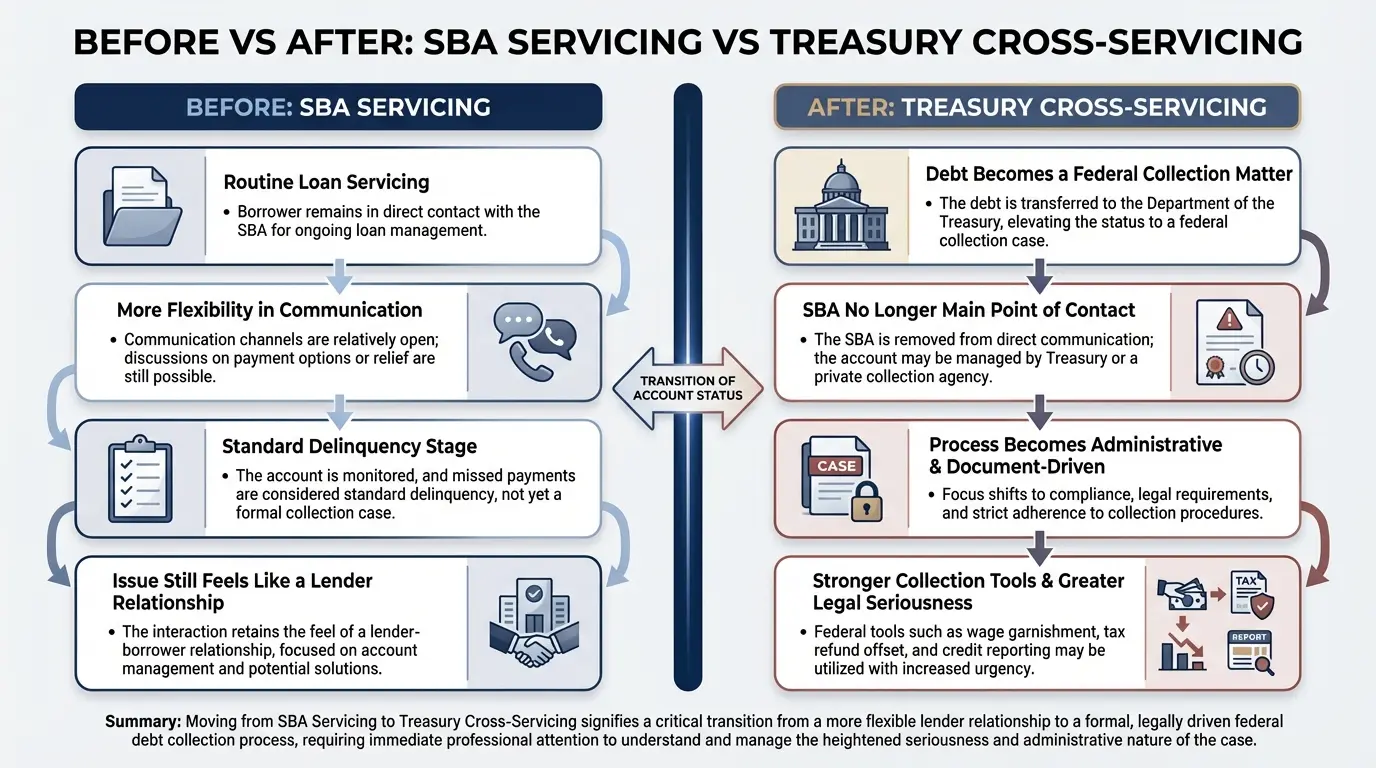

If your EIDL loan has been referred to the Treasury, you are no longer in the ordinary loan servicing stage. The Small Business Administration has recently shifted a massive volume of delinquent COVID-era relief debts into the Treasury Department’s Cross-Servicing program, changing how these accounts are managed and collected.

This transition means the SBA has stopped its routine servicing efforts and handed the matter over to federal debt collectors. The collection tools available to the government at this stage are broader and more assertive than those used during standard loan servicing.

Understanding what this shift means for your business and your personal assets is the most important step you can take right now. Taking organized, fact-based action is essential for protecting your livelihood and exploring remaining resolution options.

What It Means When an EIDL Loan Is Sent to Treasury

A Treasury referral occurs when the SBA classifies an EIDL account as severely delinquent and transfers the balance to the Bureau of the Fiscal Service. At this stage, the debt becomes an active federal collection matter rather than a standard commercial loan.

At that point, the SBA generally no longer handles the account. The borrower must now deal with a different federal collection framework.

- The SBA is no longer your primary point of contact.

- The debt is not sent back to the SBA for routine modifications.

- The process is now centered entirely on resolving a federal collection account.

What to Expect Right After the Referral

A referral to Treasury does not always feel immediate from the borrower’s perspective. There may be a gap of up to 21 days between the SBA’s internal transfer and the mailing of the first formal demand letter from the party now handling the account.

Once the debt enters Treasury Cross-Servicing, the account may be handled directly by the Treasury or assigned to a private collection agency working on the government’s behalf. Because of that, it is important to confirm who is currently handling the account before taking further action.

As the transfer processes, you should keep a few practical points in mind:

- Watch for formal notices: Demand letters will follow, providing your new account number and balance details.

- Confirm the handling party: Determine whether the Bureau of the Fiscal Service or a private collection agency is actively managing the debt.

- Use current contact information: Rely on the contact details and payment instructions in the most recent collection notice rather than older SBA servicing contacts.

What Changes Once the Loan Leaves SBA Servicing

Leaving SBA servicing means borrowers generally lose the leniency found in traditional lender relationships. Once the debt reaches the Treasury, the resolution process becomes entirely administrative and document-driven.

The government now focuses on formal debt recovery through established federal channels. Because the Cross-Servicing program handles a massive volume of federal referrals, you must stop treating the problem like a routine late-payment issue. Resolving the matter now requires submitting specific financial documentation, formal dispute forms, or structured repayment proposals.

What Can Happen After the Treasury Referral

The Treasury Department has specific administrative authority to recover delinquent federal debts. Not every collection tool is used in every case, but business owners should understand the full menu of possible actions. Many of these remedies can be deployed without the need for a traditional lawsuit.

Depending on the facts of the case, Treasury Cross-Servicing tools may include:

- Treasury Offset Program (TOP): The government can intercept federal tax refunds, certain federal benefits, and state payments.

- Administrative Wage Garnishment: Where legally applicable, the Treasury can direct an employer to withhold up to 15% of a guarantor’s disposable pay without a court order.

- Private Collection Agencies: The debt is frequently assigned to third-party contractors that specialize in federal accounts.

- Credit Reporting: The delinquency is reported to major credit bureaus, which can heavily restrict future borrowing.

- DOJ Referral: In some cases, unresolved debts may be referred to the Department of Justice for formal litigation.

Why the Balance Can Increase Quickly

After a Treasury referral, the financial obligation often expands. Federal regulations permit the government to assess administrative costs and collection fees on top of the principal and ongoing interest. Depending on the stage of collection, these added charges can steadily increase the total balance if the matter remains ignored.

Why the Loan Documents Matter More Than the Balance

Borrowers facing collection naturally focus on the total dollar amount owed. However, the language within the original EIDL loan authorization and agreement is equally important because it establishes the legal boundaries for collection.

Owners should carefully review their original paperwork for several key details:

- Borrower Entity: Whether the loan was made to a Corporation, an LLC, or a Sole Proprietorship.

- Collateral Language: For EIDL loans over $25,000, the SBA required a security interest in business assets.

- UCC Filings: Evidence of the government’s recorded interest in your business property, inventory, and equipment.

- Guaranty Terms: For loans over $200,000, the SBA required a personal guaranty, connecting the individual owner to the business liability.

Understanding these details is critical. They clarify whether the government’s collection reach is legally limited to failing business assets or whether it extends directly to your personal bank accounts and wages.

How to Assess Your Actual Risk

Assessing risk requires an objective look at your business structure and the specific terms of the EIDL loan. A borrower with a business-only obligation and no personal guaranty faces a vastly different risk profile than an owner who signed personally for a large balance.

| Factor | What to Review | Why It Matters |

| Personal guaranty | Whether one was signed and by whom | May expand exposure beyond the business entity directly to the owner. |

| Collateral / UCC filing | What business assets were pledged | May affect equipment, inventory, or other business property. |

| Borrower entity type | Sole proprietorship, LLC, corporation, etc. | Helps determine whether personal and business liability are legally separate. |

| Loan amount | Whether the balance crossed key SBA thresholds | Dictates the $25,000 collateral and $200,000 personal guaranty requirements. |

| Federal payment exposure | Whether the borrower receives federal payments or refunds | May affect the likelihood of offset-related collection activity. |

What Borrowers Should Do After an EIDL Treasury Referral

Taking proactive, organized steps is essential once a referral has occurred. This is a practical checklist to help you respond deliberately and prevent unexpected collection measures.

- Gather every recent notice: Collect all recent letters from the SBA, Treasury, and any private collection agencies.

- Identify the current servicer: Determine exactly who is handling the account right now.

- Locate original loan documents: Find your original loan authorization and note to confirm the exact terms you agreed to.

- Determine guaranty exposure: Verify whether you signed a personal guaranty based on the $200,000 threshold.

- Identify collateral exposure: Determine what business property is currently subject to a UCC filing based on the $25,000 threshold.

- Gather financial records: Prepare current business and personal financial statements before discussing any payment terms.

- Avoid hasty commitments: Do not make uninformed verbal commitments or admissions to collection agents before understanding your actual legal exposure.

Options That May Still Be Available

A Treasury referral limits some choices, but formal pathways to address the debt remain open. Public debt management guidance notes that debtors can still pursue several resolution paths depending on the circumstances.

Depending on the facts of the case, options can include:

- Debt Verification and Dispute: Borrowers have the right to submit documentation showing why the debt amount is incorrect or legally invalid.

- Payment Arrangements: Setting up a structured, negotiated monthly plan based on verified financial hardship.

- Negotiated Resolution: Submitting a formal compromise proposal if financial realities support a reduced settlement.

- Bankruptcy Review: Exploring whether federal bankruptcy protection is an appropriate way to address the debt and protect remaining assets.

The Importance of Acting Early

Addressing the debt early in the Treasury phase provides more room to navigate. Taking action before tax refunds are intercepted, wages are garnished, or the Department of Justice becomes involved gives you a much better opportunity to propose a manageable solution.

When Legal Guidance Becomes More Important

Navigating federal debt collection is quite different from working with a private bank. The rules rely on strict administrative procedures, meaning small missteps in communication or poorly timed proposals can severely limit your options.

Professional guidance becomes particularly valuable when:

- The exact scope of a personal guaranty is unclear from your memory.

- You need to clearly separate business liabilities from personal assets.

- You are preparing a formal dispute, repayment plan, or settlement proposal.

- The government has initiated a tax offset or wage garnishment that threatens your livelihood.

A careful legal analysis helps clarify your rights and ensures any response is grounded in actual federal procedure rather than guesswork.

How Penglase & Benson Can Help

Penglase & Benson provides focused legal counsel to business owners navigating complex federal debt matters. Borrowers facing Treasury Cross-Servicing often need a clear, objective assessment before making any statements to government collectors.

We can assist you by:

- Loan document review: Reviewing your original loan documents to establish the key facts and legal terms.

- Exposure assessment: Assessing your precise exposure under the $200,000 guaranty and $25,000 collateral thresholds.

Response strategy: Identifying realistic, legally sound options based on your financial situation. - Evidence organization: Helping you organize the documentation needed for a dispute or compromise.

- Agency communication: Communicating strategically with Treasury or private collection agencies on your behalf.

Our goal is to help you understand your exposure, avoid unnecessary mistakes, and choose a response strategy grounded in the facts. With clear legal guidance, you can move forward with a better understanding of your situation and options.

Visit our Contact Page to send us a message and schedule your free consultation today.

Frequently Asked Questions

What does it mean when an EIDL loan is sent to Treasury?

It means the SBA has classified the account as delinquent, stopped routine servicing, and transferred the debt to the Treasury Department’s Cross-Servicing program. The debt is now in an active federal collection status and will not be returned to the SBA.

Is dealing with Treasury the same as dealing with SBA servicing?

No. The Treasury Department handles accounts through structured administrative collection channels utilizing private collection agencies and federal statutes. They do not offer the flexible loan modifications or simple deferments previously available through the SBA.

Can the Treasury intercept tax refunds?

Yes. Through the Treasury Offset Program, the government can intercept federal tax refunds, certain federal benefits, and state payments. This offset can occur simultaneously with other collection efforts until the debt is resolved.

Can the Treasury garnish wages?

Yes. Where legally applicable, the Treasury can use Administrative Wage Garnishment to direct an employer to withhold up to 15% of a guarantor’s disposable pay. This specific federal collection tool can be implemented without needing a prior court order.

Can the balance increase after referral?

Yes. The government is permitted to assess substantial administrative costs and collection fees once the debt enters Cross-Servicing. These additions, along with ongoing interest, can steadily increase the total amount owed if the debt is ignored.

Does a personal guaranty change the risk?

A personal guaranty completely changes the collection landscape by expanding the government’s reach beyond the business entity. If you signed personally, which was required for loans over $200,000, your personal income and assets may be targeted to satisfy the debt.